Understanding Credit

What is Credit?

Credit is the ability to get goods and services before payment, based on the trust that payment will be made in the future. A credit score is a number meant to predict how likely you are to pay a loan on time, based on factors in your credit history. Credit scores range from 300-850, with a higher score being more favorable. If your credit score is lower, or you do not have a score, you may not qualify for loans or credit cards. If you do qualify, you will pay higher interest rates and fees. If your credit score is high, you will qualify for loans and credit cards and you’ll pay lower interest rates and fees, which can save you a lot of money!

Check You Credit

Three credit bureaus produce credit reports. They are TransUnion, Equifax, and Experian. You can check your credit reports from all three bureaus for free once per year at AnnualCreditReport.com. These reports won’t have your score, only a list of your accounts. You can also schedule a session with a financial coach who can pull your credit report. A credit report pulled by a financial coach at NWAF will have both your credit score and list your accounts.

5 Factors Affect Your Credit Score

- Your payment history

- The length of your credit history

- The types of credit you’re using

- Your credit utilization

- Having new credit inquiries

Rules for Building Credit

- Use a mix of credit product types to build your credit

- Always pay on time

- Use as little as possible of your available credit limit

- Maxing out your credit limit every month can hurt your score

- Be patient and know that credit building takes time

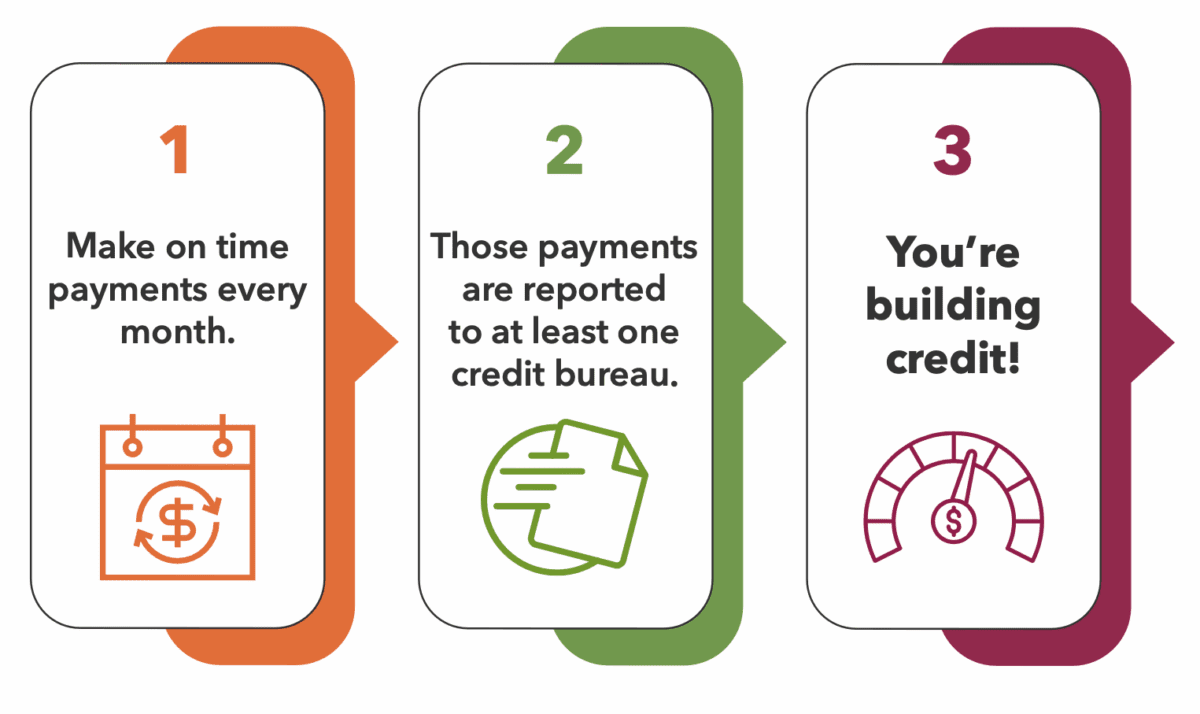

How to Build Credit

Compare Credit Products

Not all credit products are the same. Shopping around and comparing costs and features can save you money. Look for products from reputable places that have clear, written policies about repayment terms.

Smaller is better. Even you qualify for a larger loan or higher credit limit, don’t use all of it.

Make sure it’s affordable. Most credit products come with interest and fees; look for products with lower interest rates and low or no fees.

Look for flexibility. Some lenders will let you pay off debt early or work with you if you can’t make a payment.

Using Credit Cards

![]() Credit cards can be a great way to use and build credit, but they don’t work for everyone. When opening a credit card, compare interest rates and rewards. After the card is open, only use 10-30% of your available credit limit and pay off the balance in full every month. When possible, don’t max out your card or make purchases with the card because you can’t afford to pay cash. If you struggle with impulse spending, credit cards may not be a good fit for you (and that’s okay!). Only use credit cards when you know you can pay off the balance. There are other ways to build credit if credit cards don’t work for you.

Credit cards can be a great way to use and build credit, but they don’t work for everyone. When opening a credit card, compare interest rates and rewards. After the card is open, only use 10-30% of your available credit limit and pay off the balance in full every month. When possible, don’t max out your card or make purchases with the card because you can’t afford to pay cash. If you struggle with impulse spending, credit cards may not be a good fit for you (and that’s okay!). Only use credit cards when you know you can pay off the balance. There are other ways to build credit if credit cards don’t work for you.

Some content is adapted and modified from the Credit Builder’s Alliance Credit Building Toolkits.

Have questions?

If you have questions about credit, ask a coach! Click the button to ask your questions and we’ll do our best to get back to you within 3 business days. If your situation is complex, we may ask you to schedule a free session so that we can give you the best information possible. If your question falls outside our expertise, we may refer you to someone else who can help.